Website Disclosure Information – Vincents Advisory

This information is provided to assist you in deciding whether to use the financial services we offer. It includes information about other disclosure documents* we may provide to you, the remuneration we and others may receive, and what you should do if you are unhappy with our services or the products we have recommended.

Vincents Advisory Pty Ltd ABN 79 125 596 349 holds Australian Financial Services Licence (AFSL) number 320580. Our related bodies corporate are corporate authorised representatives of that AFSL:

• Vincents Private Wealth Pty Ltd ABN 63 658 402 021 (Authorised representative no. 297329)

• Vincents lifeVantage Pty Ltd ABN 88 658 133 709 (Authorised representative no. 1298411)

• Vincents Corporate Advisory Pty Ltd ABN 55 658 133 950 (Authorised representative no. 1298412)

In this disclosure information, the above four corporate entities and our employee advisers are referred to as “Vincents”, “we” or “us”.

*Disclosure documents include:

Statement of Advice (SOA), Record of Advice (ROA), Product Disclosure Statement (PDS), and Ongoing Fee Consents.

Please see below, ‘Documents You May Receive’ for information about the purpose of these documents and the circumstances in which you may receive them.

Our contact details are:

Vincents Advisory

Level 34, Santos Place, 32 Turbot Street, Brisbane QLD 4000

PO Box 13004, George Street Brisbane City QLD 4003

P: (+61) 7 3228 4000

F: (+61) 7 3228 4099

W: www.vincents.com.au

E: vincentspw@vincents.com.au

Lack of Independence

Disclosure of Lack of Independence required under 942B(2)(fa) of the Corporations Act.

s923A of the Corporations Act sets out when we can use the term independent, impartial or unbiased to describe its business. These are the four key reasons why we cannot say we are independent, impartial or unbiased:

i. When we arrange life insurance products for you, or we are listed as your adviser on a life insurance product, the Licensee will receive commission from the insurer.

ii. Our advisers may recommend financial products to you that we have a financial interest in as the issuer of or the manager of the product. Details can be found in this document under Associations and Relationships.

iii. As a licensee we restrict the financial products that can be recommended via an Approved Product List (APL). The APL includes both inhouse and external products and are selected based on a number of quantitative and qualitative factors.

iv. We receive financial benefits or soft dollar arrangements from other financial services licensees. Details of these can be provided on request. These may include stamping fees on share offers or other non-cash gifts or benefits (soft dollar arrangements).

We always put your interests before ours when giving advice but for these reasons we cannot (by law) call ourselves independent, unbiased or impartial.

Financial Services and Products we provide

We provide retail and wholesale clients with financial product advice and deal in the following financial products:

• Securities

• Managed investment schemes, including IDPS

• Superannuation

• Retirement savings account products

• Derivatives

• Deposit and payment products (including basic deposit, non-basic deposit and non-cash payment)

• Government debentures, stocks or bonds

• Life products – investment life insurance products

• Life products – life risk insurance products

• Standard margin lending facilities.

Documents You May Receive

As part of our financial advice process, you may receive:

1. Statement of Advice (SOA):

A document that explains the recommendations we provide, tailored to your personal circumstances, including the reasons for the advice, risks, and associated costs. An SOA will typically be provided when we give personal advice for the first time.

2. Record of Advice (ROA):

A streamlined version of the SOA that may be provided for subsequent advice where your circumstances have not materially changed, and the new advice is consistent with previous recommendations.

3. Product Disclosure Statement (PDS):

A document that provides details about financial products we recommend, including features, fees, benefits, and risks, to help you make informed decisions.

4. Ongoing Fee Consent:

A document that outlines the ongoing fees you agree to pay for the services provided under an ongoing fee arrangement. This document ensures you understand and approve the fees being charged, the frequency of payments, and the services you will receive in exchange for these fees.

How You Can Provide Instructions

You can provide us with instructions regarding the financial products or services we manage or recommend in the following ways:

• By Contacting Your Adviser: You can contact your adviser directly to provide instructions.

• In Writing: Email, postal mail, or fax us using the contact details provided in this document.

• By Telephone: Call our office to provide instructions. Phone: (+61) 7 3228 4000 during business hours (AEST).

• In Person: Visit our office located at Level 34, Santos Place, 32 Turbot Street, Brisbane QLD 4000.

• Through Online Platforms (if applicable): Certain instructions can be submitted via online portals or platforms where these functionalities are available.

We will confirm receipt of your instructions and may require verification or supporting documentation if necessary to fulfil your request (e.g., for large transactions or changes to your account settings).

Please note that the timeliness and execution of instructions may depend on operational or market conditions, regulatory requirements, or the nature of your request.

Remuneration we may receive

How we charge for our services

Fees are dependent upon the services provided by us to you.

Statement of Advice

There is a fixed fee for the preparation of a Statement of Advice. This will be between $1,000 and $5,000 (excluding GST). The exact amount will depend upon the complexity of the advice provided. The amount will be advised to you upon our determination of the extent of the advice. We will not undertake any further work until you have advised your acceptance of the fee.

Further Advice

When we provide you with further advice that considers your relevant personal circumstances, a Statement of Advice may not be issued. Instead, we will keep a record of the basis for that advice. You may request a copy of this Record of Advice at any time within seven (7) years from the date the advice is given by emailing your adviser.

For new retail clients, we will document your relevant personal circumstances in a Statement of Advice, along with any agreed investment strategy and advice. After that, a new Statement of Advice may only be provided if your personal circumstances or required strategy have materially changed.

General Advice and Execution-Only Services

For services that do not involve personal advice, such as general advice or execution-only transactions, fees may apply. Execution-only services involve acting on your transaction instructions without assessing the suitability of the product or strategy to your individual circumstances.

General Advice Fees: Fees for general advice are determined by the complexity and scope of the advice provided. These fees will be communicated to you prior to any service being delivered.

Execution-Only Fees: Transaction-based fees may apply for execution-only services. These fees typically include:

• A flat administrative charge, or

• A percentage fee of the transaction amount (e.g., 0.2%–0.5%).

Example:

• For an execution-only trade of $100,000, the percentage fee would equate to between $200 and $500, plus GST.

• Specific fee details, including any administrative charges, will always be disclosed to you before proceeding with the transaction.

Wealth Advisory Services

Hourly rates are applied for the provision of wealth advisory services and vary depending upon scope. In some cases, we may negotiate a fixed cost fee arrangement. In all cases, estimated fees will be provided before we commence work. Where the agreed fees are fixed the fee will be directly debited from your nominated bank account.

Portfolio Management Services

Portfolio management services fees are calculated on either a percentage or fixed basis and disclosed in a fee schedule prior to the commencement of work. Fees are comprised of:

• an ongoing fee (calculated as a percent of the funds we invest on your behalf) which ranges between 0.88% pa and 1.20% pa (excluding GST), which is deducted monthly from your investments, and

• transaction fees of 0.5% (excluding GST) of each transaction amount, which are deducted from the transaction amount.

Other Services

Fees for any other services may be payable to us or others in relation to annual accounts preparation, income tax and other annual compliance requirements associated with any structures that you may have established to hold your investments. Estimates of such fees will be provided to you prior to us undertaking work.

Commissions

Where we receive or are entitled to receive commissions, and the amount is ascertainable, we will disclose this to you in your client agreement or SOA. If the commission is not ascertainable at the time the recommendation is given, we will disclose the method of calculation of the commission and the dollar amount of the commission once we become amount of this.

We may receive commissions on certain life insurance products or other select services where this is permitted by law. These will be disclosed in detail within the Statement of Advice provided to you.

Insurance advice

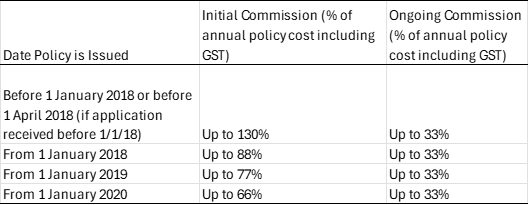

Where we arrange a life insurance product for you, the relevant insurer will pay an initial commission to us. The commission is calculated as a percentage of the premium paid (and may include health, occupational, frequency and modal loadings and policy fees, but excludes stamp duty).

Ongoing commission will also be paid when you renew your policy each year. Commissions that insurance companies pay to Vincents differ depending on when the policy commenced. These are set out in the table below:

For existing policies, the rates above will apply if you increase your cover, add new cover or otherwise amend a policy purchased by you. Please note that the initial and ongoing commissions on life insurance products are paid by product issuers and is not a direct cost to you.

We do not receive commissions for investments. Generally, we waive all entry and ongoing commission where permitted. Where we do receive commissions, we may rebate these through the investment if this option is available, unless the administration costs exceed the commissions received.

What type of research do you conduct as part of providing me with financial services?

Vincents Advisory Pty Ltd conducts up-to-date research regarding the economy, products in the investment market, product performance, the various investment markets and their respective performance, and legislative/regulatory changes.

With regard to investments, Vincents maintains a Managed Fund Approved List, which involves conducting regular due diligence on fund managers, including assessing investment processes, quality of personnel, and financial stability. Quantitative analysis is also conducted on performance and risk. Some of this research is acquired through a third party.

The Approved Product List may include related party products where applicable, and further information on the inclusion process is available on request.

A Listed Securities Authorised List is maintained using market and broker consensus data on selected ASX300 securities.

The products selected for our Managed Fund Approved List and Listed Securities Authorised List are based solely on our independent research, and no financial incentives or arrangements influence our selection. Investments on the Managed Fund Approved List or Listed Securities Authorised List are reviewed periodically as part of our regular due diligence process to ensure they continue to meet our research standards and suitability guidelines. Products that no longer meet these standards may be removed from the lists.

Investments that do not appear on the Managed Fund Approved or Listed Securities Authorised Lists (based on supported research) will not be reviewed, and therefore responsibility for monitoring such investments remains with you. If you are not under a paid fee-agreed portfolio management service, it is also your responsibility to monitor your investments.

Our advice is restricted to the products available on our Approved Product List (APL). This limitation may affect the suitability of our recommendations and means we do not provide advice on all products available in the market.

Remuneration of Vincents Advisers

Our advisers are salaried employees and do not receive commissions, fees or any other form of regular benefit or advantage arising out of recommendations made to you. Advisers may be entitled to bonuses based on performance measures including financial and non-financial indicators such as compliance with regulatory standards, client satisfaction and professional development.

From time to time, our advisers may receive non-monetary benefits (for example, attendance at conferences or training sessions) from product issuers or services providers. In accordance with our regulatory obligations, we maintain a register of non-monetary benefits exceeding $300. This register is available to you upon request.

Relationships, Associations and Conflicts of Interest

Wherever possible we avoid conflicts of interest, however where there is potential for conflict, we will disclose this to you when we make our recommendations. Please also refer to the information included above.

Your adviser may hold shares in companies or units in Exchange Traded Funds that are recommended to you, including via a Separately Managed Account that is owned and operated by the licensee.

Listed Security Authorised List and Managed Fund Approved List

Vincents may provide services to companies and fund managers who appear on our Listed Security Authorised List and Managed Fund Approved List. Where such a relationship is known, we will disclose the nature of these services at the time of making a recommendation.

Morgans Financial Limited and Acclaim Management Group Limited

Vincents may refer to Morgans Financial Limited for research and securities transactions.

Some Vincents’ directors hold an indirect interest in Acclaim Management Group Ltd, the administrator of AMG Universal Super.

Complaints and Compensation Arrangements

We are committed to providing the highest quality financial planning and investments advisory services to our clients.

If you require additional assistance with lodging a complaint with us, due to illness, financial hardship, experiencing vulnerability or where there may be literacy issues, please contact us and we can discuss how we can help.

You can raise your concerns with us in person or by letter, phone, email or facsimile, however, so the details of your complaint are fully understood and can be handled as quickly as possible by the most appropriate person, it is preferable, but not compulsory, that your concerns are made in writing.

Where a complaint relates to a particular job or service, you can direct it to the Director or Manager responsible for carrying out the work.

If you are not sure who to refer your complaint to, or you are more comfortable raising your concerns with someone you don’t normally deal with, please address your complaint to:

The Complaints Officer

Vincents

PO Box 13004, Brisbane QLD 4001

E: complaints@vincents.com.au

P: 1300 766 563

F: +61 7 3228 4099

We will endeavour to address your complaint or concern promptly. We will acknowledge your complaint within 24 hours or 1 working day verbally or via email, facsimile, or, if necessary, by mail.

Once we receive your complaint, we will initiate a thorough review of the circumstances surrounding it. We will address your concerns in a fair, objective, and unbiased manner. If additional information is required to fully assess the situation, we will contact you accordingly.

If we reach a satisfactory resolution by the end of the fifth working day after receiving your complaint, we may not provide you with a written response, unless you request a response in writing. If we are unable to meet this timeframe, we will respond to your complaint in writing no later than 30 calendar days after receiving your complaint. If this is not possible, we will write to you explaining the reasons for the delay and provide an estimated completion date for our response.

If you are not satisfied with our response, or if we do not resolve your complaint within 30 calendar days after receipt, you can take your complaint to the Australian Financial Complaints Authority (AFCA). AFCA was established by the Federal Government to help consumers reach agreements with financial firms about how to resolve their complaints. AFCA is impartial and independent. Where parties cannot resolve their complaint, AFCA will decide an appropriate outcome.

Contact details for AFCA are:

Australian Financial Complaints Authority Limited

GPO Box 3, Melbourne VIC 3001

W: www.afca.org.au

P: 1800 931 678 (free of charge)

E: info@afca.org.au

If your complaint relates to a breach of our Privacy Policy or the Australian Privacy Principles, the matter should be referred to The Privacy Officer via the contact details listed at the top of this information.

For further information about how we manage your personal data, please refer to our Privacy Policy, available at https://vincents.com.au/privacy-policy.

We have professional indemnity insurance in place and feel confident that it is a reasonable arrangement to have for compensating our retail clients for any loss or damage they may suffer should we or one of our representatives be found to have caused them to suffer loss or damage due to a breach of a relevant obligation under Chapter 7 of the Corporations Act. This complies with the requirements in section 912B and regulation 7.6.02AA of the Corporation Act.